Manchester Call Centre

Manchester Call Centre

If you are interested in borrowing money, then you may be a little overwhelmed by the wide choice of lenders in today’s market. There are many loan options from different lenders, each with their own terms and conditions from payday loans to personal loans. At Progressive Money, we understand modern life and that there may be a time you require a loan, so we’ve created a simple guide to how instalment loans work, helping you decide if they are the right option for you.

What is an Instalment Loan?

Instalment loans can refer to the majority of personal loans available to consumers that allow you to receive money that is then repaid in fixed amounts through scheduled repayments (instalments) rather than a lump sum at end of the loan term. They are often a finance solution where borrowers are able to borrow and make repayments to the loan and interest over a set period of time to suit them.

This differs from payday loans which are usually repaid in one sum around the borrower’s payday. Instalment loans may be considered a suitable option as they are more flexible in terms of repayment periods and in some cases allow you to borrow more.

However, it’s important to remember that the repayment terms, length of loan, eligibility conditions and available amounts will differ depending on the lender.

What are Instalment Loans used for?

Instalment Loans may be used for funding big purchases or emergencies that you are not able to cover the initial cost for in full.

Here are some examples of what people may use an instalment loan for:

- Buying a car

- Emergency home improvements

- Debt consolidation

- To pay off unforeseen costs and unexpected bills

- To prepare for a growing family

Advantages of an Instalment Loan

The main advantage of an instalment loan is that the repayments are spread out across the term which means the repayment amounts will be smaller and therefore are likely to be easier to manage month to month. This is helpful when it comes to budgeting as you will have a more consistent idea of your outgoings.

Instalment loans are also flexible in terms of the repayment period and most lenders will allow you to opt for a length of time to pay back the loan that will suit you. This makes instalment loans a great choice of loan for those who like to be kept in the know, as you are aware of how much you owe, when and for how long. They generally have a fixed rate of interest throughout the loan term so there won’t be any changes over time, which is great if the market rate of interest increases.

If you are approved for an instalment loan you are likely to receive the funds within a couple of days so you are able to deal with your costs or buy what you need quickly and effectively. An instalment loan could also potentially improve your credit rating if you are able to make the necessary payments on time each month.

Disadvantages of an Instalment Loan

If you agree to a longer loan term, you may find yourself making repayments with a fixed rate of interest that is now higher than the market rate. It may depend on your lender as to whether you could refinance the loan and then benefit from a lower rate of interest.

It should also be noted that an instalment loan is a financial obligation and there may be consequences if you are unable to afford the repayments in the future. This could even result in the loss of assets if the instalment loan was secured to a property or vehicle.

Are you eligible for an Instalment Loan?

The conditions of eligibility for an instalment loan will vary between each lender. The decision to lend is likely to depend on:

- How much money you intend to borrow

- How long you will be paying it back

- Your current financial situation

- Your credit rating

At Progressive Money, we always strive to consider your individual circumstances when assessing instalment loan applications rather than making a decision based solely on your credit score. In order to apply for a loan with us, you must be:

- Aged 18-70

- Employed or Self-employed

- A homeowner

- Living in the UK

- Able to afford the monthly repayments from your regular income

Whatever you’re interested in an instalment loan for, whether it’s buying a new car or paying for a home extension, if you fit the above criteria then don’t hesitate to contact Progressive Money on 0161 814 9383. Our friendly loan advisors will be happy to discuss any details around our available instalment loans and to answer any questions you may have.

To celebrate the release of the Pokémon Detective Pikachu film, Progressive Money has commissioned a study to discover the most valuable Pokémon cards of all time! You may not have managed to catch them all, but could your collection be worth a small fortune?

Although Progressive Money traditionally deals with flexible financial solutions and bad credit loans, this Pokémon infographic illustrates the wealth of potential options available when pursuing your next financial goal. So, why not check out Progressive Money’s Pokémon infographic to see if you’ve caught a fortune!

Home Improvement on a budget – 10 affordable renovation ideas

Home improvement may sound like an expensive pursuit, but there are stylish and affordable ways to makeover your house without breaking the bank. It could be that you are excited to renovate your new home or perhaps you are looking for ways to improve your property before putting it on the market. Either way, there are plenty of ideas to consider depending on your budget.

However, it is important that before you begin to approach the more cosmetic aspects of home improvement you ensure there are no major structural issues. These may be more expensive to resolve but should be prioritised before a new kitchen or redecorating. Issues such as a leaking roof, rotten joists, excessive damp or bowing walls are not only a health and safety concern but can affect the value of your home. If you are a homeowner, you may consider a home improvement loan to cover the costs.

Whether you are moving in or moving on, here are some ideas on how you can improve your home and, in some cases, even add value.

1. Make the most of your fireplace

A fireplace is a fabulous feature in any room, if you are lucky to have a period fireplace in your home why not make the most its charming character and restore it as a focal point. Over the years, many homes had the fireplace removed or bricked up, but they can be reinstated, you could even do it yourself. Replacing a marble surround may prove a bit expensive but salvaged iron combination grates can be picked up online for a few hundred pounds.

2. Freshen up your carpets and flooring

Tired carpets may need a good clean or even replacing depending on age. You can hire a professional standard deep cleaning kit and make a huge improvement to your carpet’s appearance as well as removing dirt and bacteria from your home.

If you have wooden flooring, you should try sanding and varnishing after giving them a scrub in order to get the best finish. Investing in a stylish, stair runner can also transform your hallway and make a great first impression for visitors or viewers.

3. Restore cornicing and floor tiles

Original or period features are a real asset to your home but can often become worn over time. A cornice is a decorative trim where the wall and ceiling meet and are a splendid feature in most period homes. However, you may need to strip off decades worth of paint to make the most out of the cornicing in your room. You could do it yourself, but it is a strenuous job, so it may be worth calling in the professionals.

You may also consider restoring any original floor tiles, professional cleaning will remove any old polish, wax or grime on the surface bringing their former charm back.

Whatever improvements you are making always ensure you shop around for the most competitive prices.

4. Brighten up your home

Making your home lighter can have a marvelous improvement for both yourself and potential buyers as it can create the illusion of space and is generally more appealing than a darker property. Making minor efforts such as cleaning your windows can bring in extra sunlight and installing bright, energy-efficient bulbs or light-fittings can make a huge difference to both light in the home and your bills, especially during the winter.

A skylight is a great way to transform a poorly lit room with natural light. They are usually an effective option for attic rooms and ready-made skylights are relatively easy to source and can be bought for competitive price. These improvements could contribute to adding value to your property.

5. Replace curtains or blinds

Fixing up new curtains or blinds is a great way to bring a new lease of life to a room when working with a budget. Distinctive patterns are on-trend so why not purchase a few metres of fabric and have a go at making your own curtains, the unlined panels are usually easier to make. Stylish blinds can add a lot to a room too and can be cheap to replace.

6. Get Decorating

It may sound obvious, but painting and decorating can make a huge improvement to your home and will make your property more appealing to any potential buyers as they may see your improvements as less work for them if they buy the property. If you have recently moved in, painting and decorating is also a great way to inject your personality into the property, although you may want to choose more neutral colours if you are looking to sell.

Minor odd jobs like fixing cupboards and ensuring your house looks fresh can also add value. You may also take the opportunity to increase storage space and put up some shelves. Try to take advantage of every inch of your home and have your shelves made to measure. This may require some DIY skills or the services of a bespoke furniture maker.

7. Insulate your loft

Insulating your loft may be cheaper than you imagined. Many people choose to purchase loft insulation rolls from D.I.Y stores and install it themselves. Home improvements that make your home ‘greener’ or more efficient are considered a win-win as they contribute to cheaper energy bills while you live in the home and are also appealing to potential buyers. It is worth contacting your energy supplier as many offer grants to homeowners making a step towards an energy efficient home. In many cases, home insulation can pay for itself over the years, in the form of savings made on energy bills.

8. Give your kitchen a makeover

You may want to completely renovate your kitchen by replacing all fittings, adding an island or making significant changes to layout or structure. This can be an expensive but worthwhile investment if the kitchen is in desperate need of modernising and there are home improvement loans available to help with covering the costs.

You may just want to give your kitchen a new lease of life through some smaller changes such as replacing worktops for faux marble, changing cupboard handles and the splashback behind the hob, can all contribute to the overall finish of the room. An attractive kitchen really appeals to viewers if you decide to put your property on the market.

9. Revive your front door

It’s a great idea to improve your home by painting or replacing the front door, especially if you have recently moved in as it is a fantastic way to stamp your personality on the property. Pick your favourite colour and give it a fresh coat to stand out. A really old front door may need replacing or you may even want to add a porch for some extra space.

10. Don’t forget the outside

When improving your home, you can also give the exterior a makeover. If you have recently moved then the outside may need some extra care and attention depending on the previous owners upkeeping or your landscaping tastes. It is also important if you are selling the property as the outside appearance of your home is the first thing viewers see. It’s not necessary to carry out big jobs in order to make an improvement as smaller tasks like weeding the garden, putting up fences, painting windows and garages, repairing the lawn or trimming the bushes can really make a great impression.

Ways to add value to your home

There isn’t a way to make an accurate prediction or guarantee how much your home may be worth over the next five to ten years. However, some changes can be made to your home that could improve its relative value more than others. If you plan to work your way up the property ladder, it will help to know how to maximise the resale value of your current property.

In many ways, adding value to your home is about making the most of space, whether that means a larger addition like an extension, or simply sprucing up the property with a fresh lick of paint. However, when making these home improvements you should remain aware of the ‘ceiling price’, or the maximum sale amount, of properties on your street. This means any attempts of adding value probably shouldn’t be over-ambitious in terms of cost.

Another thing to consider is the legalities of your improvements, especially with extensions or conversions. Find out if you will require planning permission and any of the associated costs before undertaking any work. It can be easy to do online at the Government website. This initial research of the process can help avoid losing vast quantities of money investing in large-scale developments, only to find out they must be undone halfway through the proceedings.

Whether you plan to put your home on the market or you want to make some improvements that could benefit you now or in the future if you do decide to sell, it is worth considering the value of your property. If you are a homeowner and plan to make some home improvements or add value to your property then you may consider a Home Improvement Loan in order to cover initial costs.

So, with that in mind, here are some suggestions that could add value to your home!

Extensions & Conservatories

Although it may not be true in all cases, more often than not when considering adding value to a property, size can make a big difference. Extensions are valuable in terms of increasing your floor space and they can be a long-term way to improve your home and potentially increase its market value. A functional extension should make it more comfortable for you to live in as the years go by rather than your family outgrowing the property.

You may also consider a modern conservatory in order to add valuable square footage to your home. Conservatories are no longer just suitable for the summer months and now can be integrated with the rest of your home in a range of styles and sizes.

Loft & Basement conversions

Loft conversions can be an excellent way to increase your living space. It may be possible to add value to your home by creating another bedroom, bathroom or even both.

You should always consider head height if you are converting a storage space into a habitable room you may need to reinforce or strengthen the floor joists which can raise the floor level. If your ceiling requires insulating it may also affect the standing room available. The space on your landing should also be thought about when planning a loft conversion as this is where the new room will be accessed and ideally you want this to look as subtle as possible. You should also research and consider any fire safety or building regulations that may apply.

Basement conversions have become an increasingly popular way to add space and value to a home, especially townhouses. However, a basement conversion is a big commitment as it will alter the structural load of the building and therefore careful thought and planning is required before making any decisions.

Turn your garage in to a living space

Although a garage can be a selling point of a home, if you don’t use your garage to park your vehicle in or to store mechanical/DIY tools then it may be worth transforming it into living space. This can completely transform the size of your home by adding an extra room. Increasing the floor space could also increase the value in comparison to other homes on your street. This home improvement is typically less disruptive than other forms of conversion, as it makes good use of existing, under used space. However, you should still consider any building regulations and contact a structural engineer to assess your foundations.

Fit a new Kitchen

If you are working with a budget when looking to add value to your home then you may want to first focus on the kitchen. As the hub of the home, it can make a great selling point of your home and can be a real deal breaker for potential buyers.

If you are redecorating or fitting a new kitchen as a way to add value before selling your home then you should try and keep it both neutral and practical in design. As always, make sure the improvements make financial sense and the cost of work is in line with the value of the home. It may be worth carrying out smaller upgrades like new cabinets or installing more modern appliances rather than completely refitting the kitchen.

Replace Windows & install a new boiler

As well as improving the aesthetic appeal of your home, replacing your windows will also create a warmer and quieter home. However, you should aim to keep the new windows consistent with the style and age of the property.

If the boiler in your home is old then it is likely that potential buyers and agents will notice. Ideally, you should have a new boiler fitted that is under warranty and this modernisation may add value to your property or at least make it more appealing to buyers as they will not need to update as soon as they buy. It may also be worth setting up smart meters, that enable you to keep track of your heating use and therefore help you to potentially reduce your household bills, or other energy efficient technology when improving your home. EPC ratings are viewed by potential buyers so trying to make your home eco-friendlier can only be a good thing.

Update your Bathroom

After the kitchen, the bathroom or bathrooms in your home are probably the best rooms to improve in terms of adding value. It is possible to make your bathroom more appealing to potential buyers without stretching your budget too far.

Your bathroom may not be in need of a new shower unit or toilet so it may be worth making some minor improvements. Updating details like changing the taps to a more modern, or stylish design could make a great difference to the room as could a new shower screen, towel rail and storage space.

Make the most of your garden

One way to potentially add value to your property is to install glass doors looking out to the garden from your living room or kitchen for example. This makes a brighter living space you can benefit from and may attract potential buyers. As well as bringing the garden into the home It can improve the practicality of your home and make it easier to entertain in the summer months.

In inner city areas, garden space can be limited so it is important to make the most out of the outdoor space you may have. You may not have a garden but why not put up some window boxes on your window sill? It can be important to make a good first impression when putting your house on the market and by making the most of every square foot of your property means you are likely to add value.

Pave a driveway

In cities or busy urban locations parking can be expensive or difficult to find, so you may want to swap a lawn for a driveway. It is worth considering whether you should sacrifice your garden space but it may be a practical option and appeal to potential buyers.

Spruce up the front & carry out small repairs

First impressions are important when it comes to the competitive property market so it is important to not neglect the outside appearance of the front of your property. In order to appeal more to viewers your home may need a fresh lick of paint where it has become tired over the years or maybe a new front door. There are smaller jobs to consider too, like cleaning the windows, unblocking the drain, weeding the path or sandblasting the driveway. As a whole, the efforts and improvements to the outside of your home make a real difference and a house that has great ‘curb appeal’ may be likely to meet its asking price.

You should try to apply this proactive approach to the small repairs inside your home too. It is important not to forget about little jobs or issues you may have grown to live with and have left unfinished when selling your home as small issues like broken light fittings or peeling wallpaper are likely to be noticed by viewers.

Bonus Tip: Hang mirrors in the hall

Hanging mirrors either side of the hallway can be a clever and cost-effective way to make a house feel larger. Although this bonus tip will not directly increase the value of your home, it will provide the illusion of space and therefore create a great first impression for viewers. However, make sure you clear the hallway first of anything that may be clutter in the space e.g. put any bikes in the shed, fold down any prams and use effective storage for shoes and coats.

How do home owner loans work?

Home owner loans are based on the value of your property, and the amount of equity you have available (equity refers to the proportion of your home that you own outright, without a mortgage). When considering a homeowner loan, you need to take into account the loan amount and repayment terms. It’s also important you check the Terms and Conditions, to see if they are suitable for your circumstances.

What is a home owner loan?

By definition, a home owner loan is secured against an owned or mortgaged property, so being a home owner is essential when it comes to taking out a home owner loan.

A home owner loan may allow you to borrow more than perhaps an unsecured personal loan. It can then be paid back over a period of time to suit your circumstances. This makes it a suitable loan option if you plan to spread cost with affordable monthly payments. However, please be aware if you are unable to pay back the loan the lender may have a right to repossess your property.

At Progressive Money we are a direct lender and have a different approach to most other lenders. We take the time to understand your situation to find the very best borrowing solution for you, without needing to secure the money against your home. We just require you to be a home owner and living in your property.

What can I use as security?

Home owner loans typically use your property as a form of security. It is not restricted to houses only, almost any type of residential property can be used, including bungalows, cottages, flats and apartments.

Are unsecured homeowner loans easy to obtain?

It is easy to apply for an unsecured home owner’s loan with Progressive Money, if you meet the following criteria:

- A home owner (you either pay a mortgage or own a property outright)

- Aged between 18 and 70*

- Either employed or self-employed

- Live in England, Scotland or Wales

- Able to afford monthly repayments

As well as your credit rating we take your personal circumstances into account in order to work out a payment plan to suit your income and situation. Our qualified team of advisors are happy to discuss any queries you may have about the application process.

How much can I borrow?

Progressive Money offer unsecured home owner loans ranging from £1,000 to £15,000 with repayment terms from 18 months to 10 years. Whether you are hoping to make some home improvements, consolidate your debts, pay for a wedding or treat yourself to a new vehicle, we may be able to help cover the cost and arrange an affordable repayment plan to suit you. As a responsible lender, we ensure that all the loans are affordable.

Use our unsecured home owner loan calculator for a no obligation quote to see how much you could potentially borrow.

Typically, a home owner loan would require you to secure against your property’s value. The amount you can borrow will depend your balance of equity, the amount left after the outstanding balance of your mortgage is subtracted from the current value of the property.

Unlike most other lenders, Progressive Money is a direct lender and only ask that you are a homeowner living in your property and can prove your eligibility for one of our loans. We may be able to offer an unsecured home owner loan, so it may not be necessary to secure against your home.

Paying back your homeowner loan

Most home owner loans are paid back in monthly instalments, often through Direct Debit. You are able to repay the loan early, however, please be aware that on settlement you will pay interest up to the date, plus one month extra.

Speak to our qualified advisors on 0161 814 9383 to discuss your loan which may be suitable for you.

Resources

https://www.money.co.uk/loans/what-is-a-homeowner-loan.htm

https://www.oceanfinance.co.uk/blog/how-does-a-homeowner-loan-work-0-5113-0.htm

How you could improve your Credit Score with 8 helpful tips

Having a bad credit rating can understandably feel quite frustrating, especially for those who are looking to apply for a mortgage, car loan or other forms of finance.

If that sounds familiar, you’ll be pleased to hear that there are measures you can take to gradually improve your circumstances and credit score. You’ll also be pleased to hear that we offer a range of Bad Credit Loans to our customers, perfect for those who may need to borrow up to £15,000 who may have been refused by other lenders.

With these 8 tips you could improve your credit score and leave your old rating behind

Track your credit score

Some credit report services charge a fixed or membership fee to track or request your credit report. In recent years, however, many of these companies have changed their practices, instead offering a free service or opting to recommend credit cards and other offers on their websites instead of a credit check fee.

To you, this simply means that you can track your credit rating for free, as well as receive recommendations from the service on more ways to improve your credit record. Free services generate monthly reports, allowing you to track your credit rating improvements in real-time.

Space out applications for credit

While credit reference agencies aren’t necessarily told if you’re rejected for credit, they are able to see the frequency of applications you make and whenever a search is made by a lender.

Simply put, don’t apply for credit in quick succession. If possible, find out if you are likely to be accepted for a new line of credit before applying to avoid credit checks being made unnecessarily.

Close unused credit cards and other accounts

Lenders often take more than just the amount you currently owe into consideration when checking your eligibility for finance, they often also consider the amount of credit you have access to. This can be unused credit cards, store credit cards and even mobile phone contracts.

While you may not necessarily owe money to these dormant lines of credit, the access is still there, and there is potential to borrow more in the eyes of prospective lenders. To rectify this, close unused lines of credit and finance, and check for active but unused services such as old mobile phone contracts.

Cut financial ties

Having a ‘financial partner’ who has a bad credit score may bring your joint-score average down by association. This could be in the form of still having a joint bank account or a joint mortgage with an ex-spouse following a divorce.

These financial links may impact your own credit rating, so if there is an opportunity to do so, maybe it’s worth cutting financial ties. If this is an option, be sure to inform the appropriate credit reference agencies of the disassociation to ensure the other person’s financial history and future dealings could reduce the impact on your credit score.

Register on the electoral roll

The electoral roll allows lenders to validate your stated place of residence, subsequently improving your chances of being eligible for credit.

Living at the same address, maintaining the same bank account and working for the same employer for at least a 12-month continuous period may also help improve your credit score.

Ensure all future repayments are made on time

Missed or late repayments can appear on your credit record for up to six years, so it’s crucial that you make all of your outstanding credit repayments on time. This can also apply to late payments on utility bills such as gas or electricity.

Pay off outstanding debts as soon as possible

Paying off your debts ahead of schedule may also help improve your credit score as this shows that you’re making a proactive effort to repay what you have borrowed.

If you’re able to set aside a small budget each month to pay off debt, it will certainly pay-off in the long term (no pun intended!).

Use credit to build a history

For some people, it’s maybe not a ‘bad’ credit history that prevents them from being eligible for credit, it’s a lack of credit history. Some lenders are reluctant to lend to those who have no credit history whatsoever, as they’re unable to see if they’re likely to make repayments on time or not. Using credit sources like credit cards in a sensible manner can help build a positive credit history.

For example, using the card to purchase essentials that you would otherwise still purchase (such as a monthly train pass or food shopping, keeping to your usual budget) and then paying off the full outstanding amount each month with a direct debit.

So there you have our 8 tips to credit score recovery Remember, improving your credit rating is a gradual process, and requires ongoing care and attention. If you’re looking to borrow money and currently have a poor credit rating, you might like to view our range of bad credit loans.

How to enjoy a summer festival without spending too much

The UK’s immensely popular festivals attract to their stages once-in-a-lifetime performances and some of the biggest names in music every year. It’s little wonder the scene continues to go from strength to strength.

The music festival has been a mainstay in the British summer schedule since a boom in popularity in the early 1980s and its soaring status has meant that for many, it’s seen as a replacement for a summer holiday. Music lovers eagerly look forward year-round to the multi-day events, which, actually, don’t cost that much less than an average summer break. So how much are we really spending on this rather pricey weekend away?

What’s the cost of a summer music festival?

You’d be forgiven for thinking you’d need to take out a loan to attend a music festival in 2018. When you factor in ticket prices, food and drink, camping equipment and travel costs, it all adds up to an expensive weekend of fun.

Over the last 10 years, Progressive Money found the price of a ticket alone has risen by 66% and will now set you back an average of £164 for a weekend. This year, five of the UK’s biggest festivals are charging more than £200 for a ticket. This is a staggering increase when compared to 2008, when ticket prices hovered around the £100 mark. A decade ago £155 for Leeds and Reading Festival was the most you’d expect to pay, whereas now a single weekend ticket would cost £205 exclusive of fees.

But what about those added extras? If you’re going through a booking site for tickets, you can expect to pay up to 8% per ticket* for booking fee alone, as well as service charges and postage costs. All this makes for an incredibly expensive ticket price, even when compared to the steep face value. Such an initial outlay can massively eat into your budget for the weekend. That’s not all. Festival-goers need to ensure they have the proper kit to weather the elements while camping in a huge field. A tent, sleeping bag, pillow, airbed or mat – this little lot will set you back an average of £81.60.

So how can you do a summer music festival on a budget?

If you’re keen to attend one of the UK’s many festivals this year, there are ways you can do it without breaking the bank or having to re-mortgage the house. To give you a nudge in the right direction, we’ve taken a look at the clever ways you can keep costs down without compromising on the experience:

- Buy tickets together. If you’re going with a group of friends, buy all the tickets at the same time. Yes, each one will still carry a booking fee, but you’ll dodge a sizeable chunk of the service charge and extra postage if all the tickets are sent out together.

- Equipment. An easy one – take care to look after your camping gear and you’ll avoid having to fork out for new equipment each year. However, if you do find yourself needing to buy new, check out second-hand websites and local lists for cheap deals.. Better still, borrow from friends and family.

- Take your own. This applies to absolutely everything. Food and drink at UK festivals can be extortionate, but most of them will allow you to bring your own. Check out each festival’s rules and policies to find out what you’re allowed to bring.

- Budget. Draw up a plan and stick to it. Spending while you’re at a festival can quickly spiral out of control without you realising, so set yourself a strict budget before you go. Don’t spend more than you can afford to.

- Volunteer. Some festivals offer free tickets, providing you’re willing to do a little bit of work in return. You can earn your freebie by working at the bar, clearing up after the event or directing people around the site. This could be a small price to pay to see your favourite bands live and get up close to all the action.

- Ticket types. You may not have to pay full price – it’s worth looking into. If you’re attending the festival with students, teenagers or children, you may be able to get concession tickets. There are often much cheaper alternatives available and children’s tickets are often free.

Follow these top tips for summer savings and you could slash the cost of your festival weekend. That way you’ll remember it for all the right reasons and not have to dread the monthly bank statement coming in. You don’t always have to pay through the roof to have a great summer experience.

*maximum cumulative booking fee for UK’s top five music festivals when booking via official providers.

It’s the start of a new year and that means it’s a great time to take a fresh look at your finances. If you’ve resolved to be more savvy with your money in 2018 now is the time to get saving.

The first step to saving money

is to take a cold hard look at your incomings and outgoings to make cuts (it often starts with shop-bought lunches) and plan a budget.

Over half of UK households keep a regular budget. Most say it gives them peace of mind about how much they are spending and makes them feel better about life in general.

To get started on your budget, you’ll need to work out how much you spend on:

- Household bills

- Living costs

- Financial products (insurance…)

- Family and friends (presents…)

- Travel (car costs, public transport…)

- Leisure (holidays, sport, restaurants…)

Keep a Track on your spending

If you’re spending more than you have coming in, you need to work out where you can cut back.

This could be as easy as making your lunch at home, or cancelling a gym membership you don’t use.

You could also keep a spending diary and keep a note of everything you buy in a month.

Or, if you do most of your spending with a bank card, look at last month’s bank statement and work out where your money is going.

Alternatively, you can set up a budget using a spreadsheet or just write it all down on paper.

Free Apps available

There are also some great free budgeting apps available and your bank or building society might have an online budgeting tool that takes information directly from your transactions

Haggle on household bills

Haggling might sound daunting but Which? research shows you can save around £725 a year just by questioning the price of your household bills. In October 2017, Which? surveyed more than 2,000 people about their haggling experiences and 58% said they had negotiated sizeable discount. There are also savings to be made on car insurance, home insurance, car breakdown cover, mobile, broadband & pay TV and energy bills.

Automate your savings

It’s easy to use all the extra money you free up in your budget on extra treats rather than saving it. But there are more and more ways to get into the savings habit without actually doing much. There are a few free automated savings app that monitors your spending habits, works out what you can afford to save and siphons what you can spare out of your account. So why not check with your bank to see if they have this app facility available.

Get into the cashback habit

If you shop online, you should try to get into the habit of using cashback websites to save every time you make a purchase. When you shop using the many cashback websites available, you can earn a percentage (typically 1%-15%) of what you spend back. Quidco estimates members earn £305 back each year while Top Cashback claims members amass a whopping £356 per year with this simple shopping trick.

Join more loyalty schemes

Loyalty schemes that are free to join are a great way to rack up savings as you spend. Most of us will have supermarket loyalty cards like the Tesco Clubcard or the M&S Sparks card but there are lots more schemes you might not have heard of that can help you build up points that turn into vouchers or give you access to freebies. Asos A-List, The Body Shop Love Your Body, the Nando’s Card, my John Lewis, IKEA Family and Boots Advantage these are just some of the loyalty cards available.

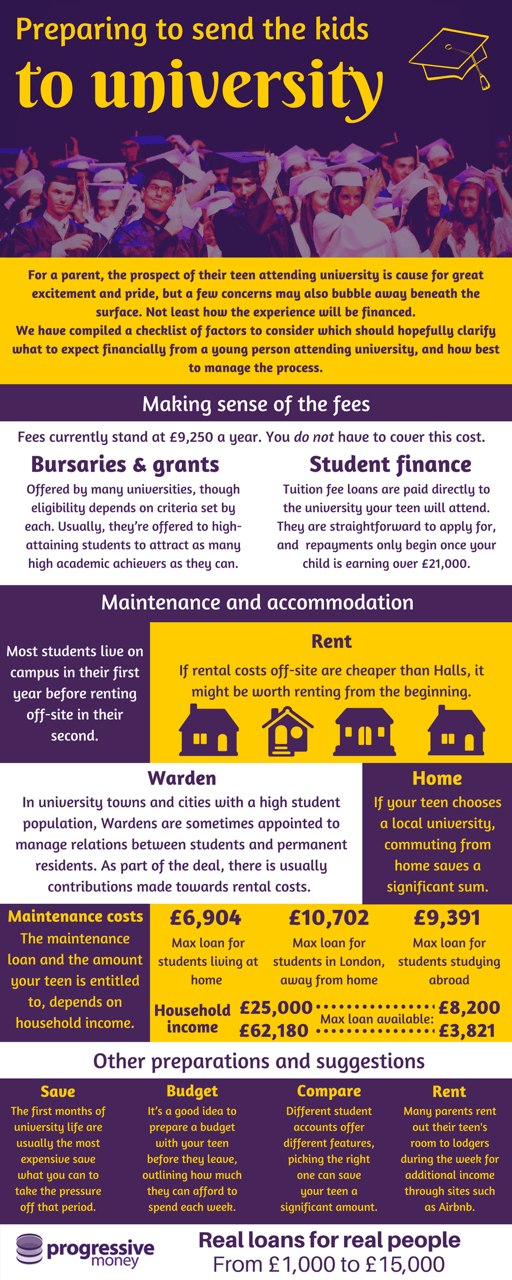

If you have a teenager aged 15-16 who is performing well academically, you’ll no doubt be having thoughts about what the future holds for them in terms of further education. ‘University’ is a word that has probably crept into the family lexicon on more than one occasion. For a parent, the prospect of their youngster attending university maybe cause for great excitement and pride, but a few concerns may also bubble away beneath the surface. Not least how the experience will be financed.

For those of you who read the above with an uneasy familiarity, fear not. We have compiled a checklist of factors to consider which should hopefully clarify what to expect financially from a teen attending university, and how best to manage the process.

Making sense of the fee

Few will have forgotten the government’s tripling of university fees in 2012 and the subsequent political bar brawl that followed. Five years on, it’s still a sore topic and despite the convictions and protestations of many, the fees remain, at many universities, at an eye-watering £9,250 per academic year. However, these fees do not have to be paid up front from your own cash reserves. There are two alternatives:

Bursaries and grants

As your teen begins to zero in on the universities they’d like to attend, have a look at the websites of each. Many offer grants and bursaries, though eligibility for these depends on criteria set by each institution. In most cases, they’re offered to high-attaining students as a means of attracting as many highest academic achievers as they can.

Obviously, your youngster is 100% motivated towards academic excellence and needs no further kickers, but on the off-chance an extra carrot wouldn’t go amiss, the possibility of financial support for their efforts might be worth whispering in their ear.

Student finance

Tuition fee loans come as part of the Student Loan package and are paid directly to the university your teenager will attend, never settling in their account. They are straightforward to apply for, and your teen will only begin making repayments once they’re earning over £21,000.

The fees then, despite initially looking a little terrifying, can be met with some dedicated form-filling. Accommodation and maintenance costs though, may take require a bit more stretching of the grey matter.

Maintenance and accommodation

The Student Loan is essentially split into two parts; tuition and maintenance/accommodation. We’ll begin with the accommodation side of things.

Accommodation costs

keeping a roof over your teen’s head during their university life can be expensive business, so let’s look at some options.

Firstly, it’s worth pointing out that most students spend their first year of university living on campus, before moving into rented accommodation in their second year in the nearby town or city. However, consider the following:

Renting: Once your teen has been accepted into a university, it might be worthwhile looking at rental costs in the local area. If there’s significant discrepancy between halls of residence and rented accommodation, it might be something worth exploring.

Proximity to home: It may well be that your teen is eager to put as much distance between themselves and you as possible during their studies (don’t take it to heart), but there’s also every chance they’re looking at universities closer to home. Should that be the case, commuting from home to classes could save a significant amount.

Catering: If your teen is headed for halls of residence, have a look at the catering that’s offered. Going for a catered option will ensure they are being fed proper meals, you’ll just need to decide whether it will be more or less expensive than your teen sourcing their own food.

Warden:In university towns and cities with a high student population, Wardens are sometimes appointed to manage relations between students and permanent residents. The role is multi-faceted and involves liaising with various bodies and groups, but as part of the deal, there is usually contributions made towards rental costs. There are no guarantees your teen will be successful in applying to be a Warden, but if they’re up for the challenge, the rental contributions can be quite the incentive.

Maintenance costs: Linked to accommodation costs are general maintenance costs. These are covered by the maintenance loan and the amount your teen is entitled to, depends on household income. The maximum that can be claimed is £8,200 per academic year for households on an income of £25,000 or less. The figure reduces the higher the household income as this table illustrates:

| Household income | Loan entitlement |

| £25,000 | £8,200 (max loan) |

| £30,000 | £7,612 |

| £35,000 | £7,023 |

| £40,000 | £6,434 |

| £42,875 | £6,095 |

| £45,000 | £5,845 |

| £50,000 | £5,256 |

| £55,000 | £4,667 |

| £60,000 | £4,078 |

| £62,180 | £3,821 (min loan) |

| £65,000 | £3,821 |

| £70,000 | £3,821 |

Other important figures to consider are:

- £6,904 – maximum loan for students living at home while studying/li>

- £10,702 – maximum loan for students living in London and away from home

- £9,391 – maximum loan for students living or studying abroad for at least one term

Other preparations

Away from grants, bursaries and loans, there are a few things you and your teen can be doing, or can do once studies commence, to lighten the financial load.

Save!

Saving in advance borders on the imperative for a soon-to-be student and their parents. The first few months of university life are usually the most expensive, so even if you’ve left it late, save what you can to take the pressure off that period.

Compare student bank accounts

For most students, their student bank account will be at the epicentre of their financial world whilst at university. Different student accounts offer different features and picking the right one can save your teen a significant amount over the duration of their studies.

Some student accounts also offer other incentives like travel insurance or a student railcards that may prove useful and save your teen money during their university life.

Prepare a budget

Simple lack of experience means young people generally have little concept of managing money. In fact, for many students, their first maintenance instalment will be the most money they’ve ever seen in a bank account that belongs to them. This can spell danger if not met with parental guidance. Before they leave, organise a little sit-down and work out:

- What their major costs will be while at university

- What you as parents/carers can afford to contribute

- Any other income they will have such as wages from a job

It’s a good idea to then prepare a budget with them before they leave, outlining how much they can afford to spend each week. If preparing an effective budget is proving a challenge, it is worth remembering that UCAS, in association with the Money Advice Service, provide advice and assistance with this.

Consider renting out their room

This might seem drastic, but is actually becoming quite common. Sites such as Airbnb allow users to advertise rooms to lodgers who may only need somewhere to sleep during the week. This means your teen’s room is available should they want it at the weekend, and you can bring in a few extra pound coins while they’re away.

Ever since the first ancient Assyrian and Babylonian merchants began lending grain to the farmers and traders of the time, human beings have been lending forms of currency to each other for a fee.

The journey the lending industry has undertaken since then has been colourful to say the least. Often maligned in literature through Scrooge type characters, preyed upon by shadowy loan sharks quick to use intimidation as a penalty for late payments, and even getting mentions in the Bible.

As with most industries, however, the complexion of the industry has changed beyond recognition with the onset of technology and robust regulation. Borrowing has not gone away, and the basic transaction remains the same with one party providing capital for another, for it to be paid back with interest. How borrowers acquire capital, how they pay it back, and their reasons for needing it though, have all changed dramatically.

Why we borrow

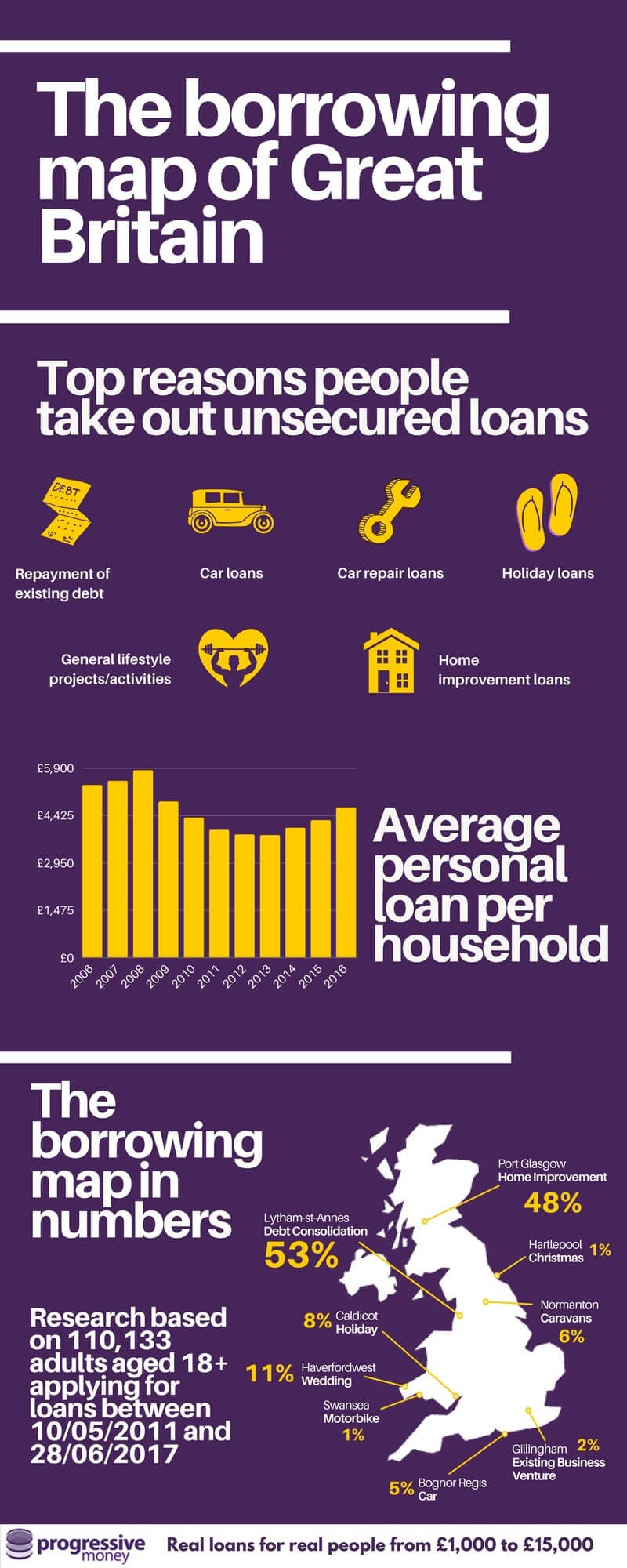

In the past, loans were taken primarily as a means of survival, be it for land, livestock, even simply for food. As civilisation has evolved, so have our needs for emergency capital. Perhaps the most interesting development has been the loan to pay off debt. Outstanding liabilities would once have precluded a person from qualifying for a loan. Today the flagship product of many companies is one which consolidates all owed monies into one payment, usually to be returned in monthly instalments. Illustrating this trend well, Darwin Group, which incorporates Progressive Money, recently undertook a survey of over 110,000 people from across the UK. In Lytham St Annes, over half (53%) of respondents cited debt consolidation as their reason for taking out an additional loan.

The technology we depend on also features high amongst the reasons people go to official third parties for capital. Cars and computers are now commodities few can function without and they often need replacing and repairing. Unfortunately, these commodities rarely give warnings when they need to be replaced or repaired, and the cost of both can be high -necessitating the need for a loan.

Perhaps a cheerier trend which has developed has been that of people taking out loans not so much out of desperation, but to finance more exuberant purchases. Amongst the top reasons people now borrow, is to finance holidays and an array of general lifestyle pursuits and projects. Linked to this are monies borrowed to make home improvements. Indeed, the Darwin survey discovered that 48% of those questioned in Port Glasgow, had taken out loans to spruce up their homesteads.

Beyond these, paying for Christmas and caravans all featured as reasons Darwin Group found for people turning to loans, with 11% of smitten folk from Haverfordwest borrowing to pay for their weddings.

How much are we borrowing?

The average household loan was increasing steadily from the turn of the millennium before topping at almost £6,000 in 2008. In 2009 that figure fell sharply to around £5,000. Few people will need reminding what happened around that time. The ‘credit crunch’ as it became widely referred to, saw a contraction in spending for most people and most industries. The reason for the dip in borrowing was most likely two-fold, with people unwilling to take on more debt in an uncertain economic climate, and loan companies reluctant to lend money, similarly fearing the country’s financial predicament. The value of household loans continued to drop before plateauing in 2012/13 at around £4,000. Since then, there has been a gradual increase, and the average loan now stands at comfortably over £4,500.

Where do we turn when the bank says no?

The ‘computer says no’ phenomenon is all too familiar for people trying to acquire capital when their credit scores are not the best. Fortunately, there are other options. Progressive Money, a subsidiary of Darwin Group, offer a degree of flexibility that rival companies struggle to match. Offering unsecured loans of up to £15,000, over terms of up to ten years, they accept customers with recent defaults or CCJs, who’ve missed mortgage payments within the last 12 months, and will lend to benefits claimants and the retired, typically transferring funds within three days. Progressive by name, progressive by nature.

Socialise

Progressive Money Limited is a direct lender and licensed credit broker. If your application for a loan doesn’t meet the underwriting requirements of Progressive Money Limited or you wish to consider other lending options, we may with your permission, pass your information onto other selected third party lenders or brokers, including other group companies. Authorised and regulated by the Financial Conduct Authority. Firm Reference No. 690699. Registered with the Information Commissioners Office No. Z3414982.