Manchester Call Centre

Manchester Call Centre

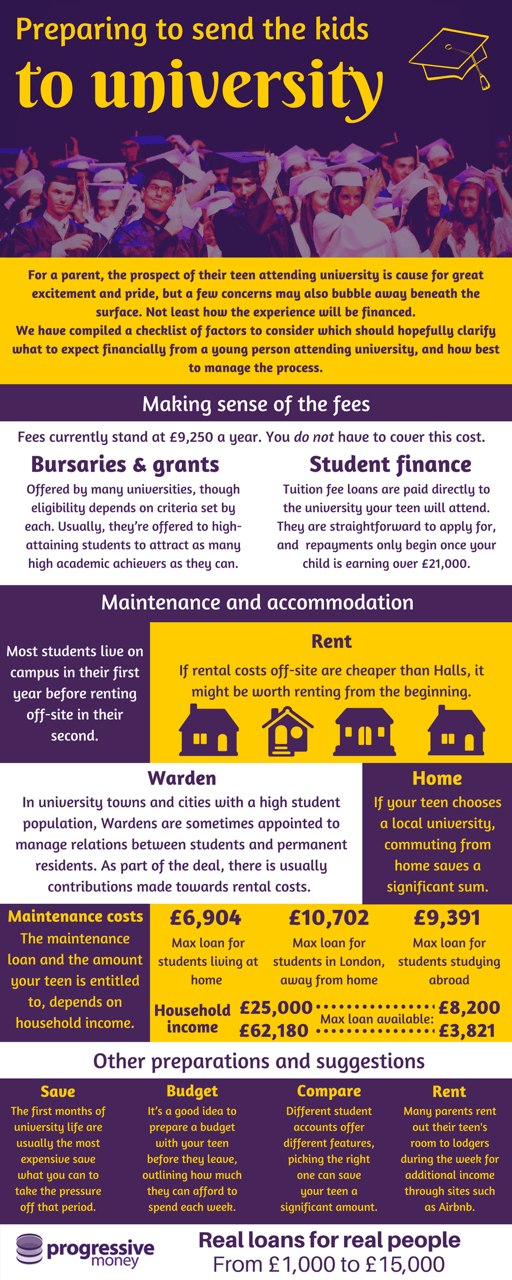

If you have a teenager aged 15-16 who is performing well academically, you’ll no doubt be having thoughts about what the future holds for them in terms of further education. ‘University’ is a word that has probably crept into the family lexicon on more than one occasion. For a parent, the prospect of their youngster attending university maybe cause for great excitement and pride, but a few concerns may also bubble away beneath the surface. Not least how the experience will be financed.

For those of you who read the above with an uneasy familiarity, fear not. We have compiled a checklist of factors to consider which should hopefully clarify what to expect financially from a teen attending university, and how best to manage the process.

Making sense of the fee

Few will have forgotten the government’s tripling of university fees in 2012 and the subsequent political bar brawl that followed. Five years on, it’s still a sore topic and despite the convictions and protestations of many, the fees remain, at many universities, at an eye-watering £9,250 per academic year. However, these fees do not have to be paid up front from your own cash reserves. There are two alternatives:

Bursaries and grants

As your teen begins to zero in on the universities they’d like to attend, have a look at the websites of each. Many offer grants and bursaries, though eligibility for these depends on criteria set by each institution. In most cases, they’re offered to high-attaining students as a means of attracting as many highest academic achievers as they can.

Obviously, your youngster is 100% motivated towards academic excellence and needs no further kickers, but on the off-chance an extra carrot wouldn’t go amiss, the possibility of financial support for their efforts might be worth whispering in their ear.

Student finance

Tuition fee loans come as part of the Student Loan package and are paid directly to the university your teenager will attend, never settling in their account. They are straightforward to apply for, and your teen will only begin making repayments once they’re earning over £21,000.

The fees then, despite initially looking a little terrifying, can be met with some dedicated form-filling. Accommodation and maintenance costs though, may take require a bit more stretching of the grey matter.

Maintenance and accommodation

The Student Loan is essentially split into two parts; tuition and maintenance/accommodation. We’ll begin with the accommodation side of things.

Accommodation costs

keeping a roof over your teen’s head during their university life can be expensive business, so let’s look at some options.

Firstly, it’s worth pointing out that most students spend their first year of university living on campus, before moving into rented accommodation in their second year in the nearby town or city. However, consider the following:

Renting: Once your teen has been accepted into a university, it might be worthwhile looking at rental costs in the local area. If there’s significant discrepancy between halls of residence and rented accommodation, it might be something worth exploring.

Proximity to home: It may well be that your teen is eager to put as much distance between themselves and you as possible during their studies (don’t take it to heart), but there’s also every chance they’re looking at universities closer to home. Should that be the case, commuting from home to classes could save a significant amount.

Catering: If your teen is headed for halls of residence, have a look at the catering that’s offered. Going for a catered option will ensure they are being fed proper meals, you’ll just need to decide whether it will be more or less expensive than your teen sourcing their own food.

Warden:In university towns and cities with a high student population, Wardens are sometimes appointed to manage relations between students and permanent residents. The role is multi-faceted and involves liaising with various bodies and groups, but as part of the deal, there is usually contributions made towards rental costs. There are no guarantees your teen will be successful in applying to be a Warden, but if they’re up for the challenge, the rental contributions can be quite the incentive.

Maintenance costs: Linked to accommodation costs are general maintenance costs. These are covered by the maintenance loan and the amount your teen is entitled to, depends on household income. The maximum that can be claimed is £8,200 per academic year for households on an income of £25,000 or less. The figure reduces the higher the household income as this table illustrates:

| Household income | Loan entitlement |

| £25,000 | £8,200 (max loan) |

| £30,000 | £7,612 |

| £35,000 | £7,023 |

| £40,000 | £6,434 |

| £42,875 | £6,095 |

| £45,000 | £5,845 |

| £50,000 | £5,256 |

| £55,000 | £4,667 |

| £60,000 | £4,078 |

| £62,180 | £3,821 (min loan) |

| £65,000 | £3,821 |

| £70,000 | £3,821 |

Other important figures to consider are:

- £6,904 – maximum loan for students living at home while studying/li>

- £10,702 – maximum loan for students living in London and away from home

- £9,391 – maximum loan for students living or studying abroad for at least one term

Other preparations

Away from grants, bursaries and loans, there are a few things you and your teen can be doing, or can do once studies commence, to lighten the financial load.

Save!

Saving in advance borders on the imperative for a soon-to-be student and their parents. The first few months of university life are usually the most expensive, so even if you’ve left it late, save what you can to take the pressure off that period.

Compare student bank accounts

For most students, their student bank account will be at the epicentre of their financial world whilst at university. Different student accounts offer different features and picking the right one can save your teen a significant amount over the duration of their studies.

Some student accounts also offer other incentives like travel insurance or a student railcards that may prove useful and save your teen money during their university life.

Prepare a budget

Simple lack of experience means young people generally have little concept of managing money. In fact, for many students, their first maintenance instalment will be the most money they’ve ever seen in a bank account that belongs to them. This can spell danger if not met with parental guidance. Before they leave, organise a little sit-down and work out:

- What their major costs will be while at university

- What you as parents/carers can afford to contribute

- Any other income they will have such as wages from a job

It’s a good idea to then prepare a budget with them before they leave, outlining how much they can afford to spend each week. If preparing an effective budget is proving a challenge, it is worth remembering that UCAS, in association with the Money Advice Service, provide advice and assistance with this.

Consider renting out their room

This might seem drastic, but is actually becoming quite common. Sites such as Airbnb allow users to advertise rooms to lodgers who may only need somewhere to sleep during the week. This means your teen’s room is available should they want it at the weekend, and you can bring in a few extra pound coins while they’re away.